Home

HomeHow Small Businesses and Startups Can Navigate the Current Hard Economic Times

Our modern world is a global marketplace, a web extending throughout every country and region. When economic activity rises or falls somewhere, there is a ripple-effect spanning the global economy.

China’s slowdown caused by the COVID-19 outbreak and subsequent spread of the virus affected many industries and companies in developing and emerging nations, even the virtual world-based IT industry. Europe’s previously borderless economic union started shutting borders, disrupting some of the largest global economies. Now, the pandemic has plunged the United States into a recession, with 38 million unemployed as of the end of May 2020. It’s hampering global economic growth, markets are dropping, and people around the world are preparing for a lengthy economic downturn.

The impact of recession on businesses may vary depending on the entity size. As a small outsourcing company developing software solutions primarily for small and middle-sized enterprises (SMEs), we are concerned about its possible impact on small businesses. We are also thinking about how we, along with our clients, should navigate through this crisis to come out stronger on the other side.

The understanding of how economic factors affect business is essential, so let’s start with the basics: what does recession mean in business terms?

Definition of an Economic Recession

One popular definition is two consecutive quarters of declines (negative growth) in the gross domestic product (GDP). The National Bureau of Economic Research (NBER) defines a recession as a “significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

Others are defining a recession based on the signs of a general decline in the stock market over some time. For example, the last such period roughly coincided with the Great Recession that officially lasted from December 2007 to June 2009. Such predictors and indicators are critical for investors and business decision-makers.

One of the primary indicators and effects of recession is a massive loss of jobs. As sales revenues and profits decline, companies reduce headcount and either slow or freeze hiring. This further slows down the economy.

A recession changes customers’ purchasing attitudes, driving companies to lower their prices or clear smaller volumes. In an effort to cut costs and improve the bottom line, they may stop buying new equipment, curtail research and development, postpone new product rollouts, compromise the quality of their products, and cut their marketing and advertising expenditures. Such efforts by big companies impact others, both large and small, that normally supply goods and services for the activities affected by cost-saving. Business owners up and down the supply chain make fewer sales and may even be forced into bankruptcy. A rash of business and bank failures is typical for recessions. As these effects ripple through the struggling economy, consumer confidence, and hence, spending declines, perpetuating the recession.

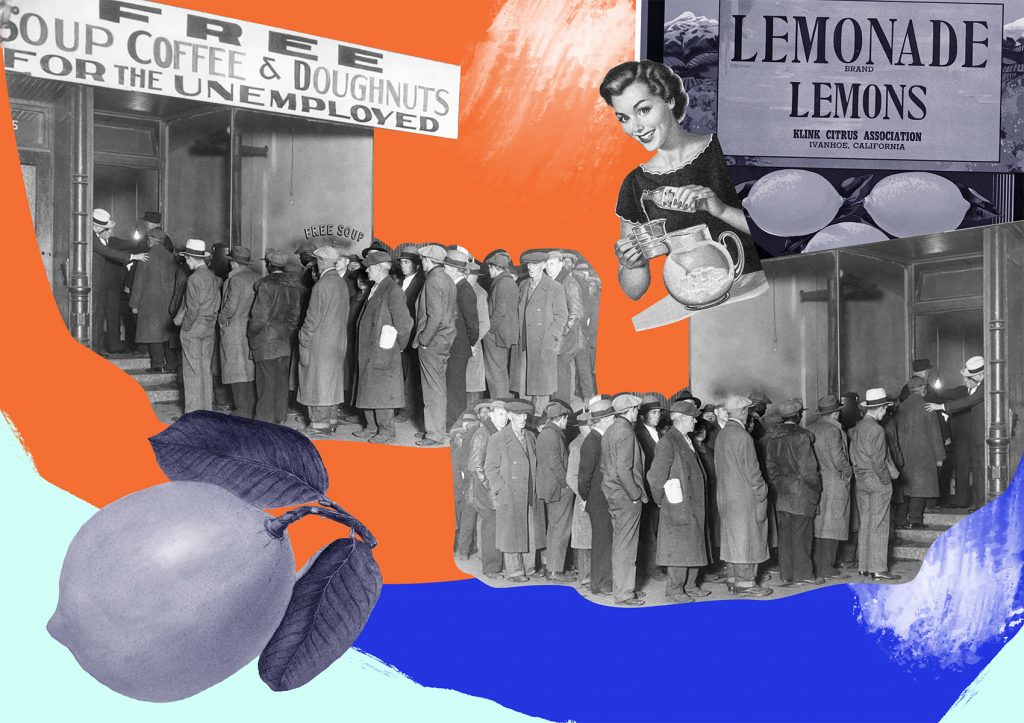

A recession that lasts longer, years, not months, and has a much worse overall impact, is called a depression. For example, the Great Depression started in 1929 and lasted through 1933. It originated in the U.S., where the unemployment rate had touched 25% and the GDP fell by 30%, and caused a worldwide economic downturn that lasted until World War II.

However adverse recessions may be towards countries, industries, enterprises, and employees, they are a normal and unavoidable part of the economic cycle. In the past one hundred years, there have been 17 recessions, which means they occur roughly every six years. According to NBER data from 1945 to 2009, the average recession lasted eleven months. However, it’s difficult to predict when the next one happens and how severe it will be, because the causes and the impact on various industries can vary. In 2019, with the Great Recession still fresh in our minds, the next one had been predicted to begin by the end of 2021 or even by March 2021. However, COVID-19 struck sooner.

The spread of the virus and public health lockdowns exemplify the type of economic shock that can trigger a recession. The coronavirus crisis is likely to create a U-shaped or even W-shaped recession, where the economy plunges, starts to grow, and then drops again. Some economists even fear that it has a depression potential.

What shall SMEs expect from the globalized economy now? How does the economy affect businesses in this category?

The Impact of Recession on Businesses

Small and middle-sized businesses often feel the effect of economic changes faster than their larger counterparts.

During an economic downturn, when people lose their jobs or become concerned about their job stability, they cut back spending. Entities also become increasingly cautious with expenditures, which leads to decreased revenue for SMEs. Many companies are forced to downsize their workforce, hampering their ability to serve customers. A slow profit stream can make it challenging to repay creditors and negatively impact a company’s viability. Credit markets become tighter and banks start increasing their lending restrictions (this is known as “credit crunch”). A struggling business is less likely to receive loans for capital expenditures and operations, which limits their growth potential.

Without significant cash reserves and capital assets, and less likely to secure additional financing, SMEs may have a harder time surviving a recession. As a result, bankruptcies occur more often among them than among large companies which are often eligible for government bailouts and special loan arrangements.

A downward economic cycle can severely impact most SMEs, but some can thrive and even grow during hard economic times. For example, companies facilitating home foreclosures and vehicle and property repossessions would find their businesses on an upswing. B2C and digital businesses may be less impacted and generate higher profits as well. And all SMEs may take advantage of new opportunities. For example:

- There will be less competition in the market, because vulnerable or obsolete firms will go out of business, and fewer entrepreneurs will invest venture capital when the economy is ailing.

- Buy-side Merger and Acquisition opportunities may emerge not only for big companies. With substantial financial backing, SMEs may seize expansion opportunities: take over customer bases of out-of-business competitors and buy out struggling ones.

- Customers that you onboarded during the trying times, provided discounts and a lending hand, and helped to grow through the tough times, are more likely to stick with you when things change for the better.

- SMEs can save on overhead expenses, such as rent, office furniture, electronics, or materials they may get at a discount or buy from businesses that are closing or needing to reduce inventory.

- A recession is an opportunity to identify vulnerabilities and improve everything. During a weaker economy, it’s easier to justify investments in infrastructure and technical debt. Slower sales cycles even allow for the opportunity to switch from an obsolete technology to something more progressive and capable of scale.

It’s hard to forecast just how long the current crisis will last, but it is sure to have a significant impact on small businesses in the months ahead.

Let us share some proven advice that we hope will help you make smart decisions and prosper during the economic downturn.

Things to Focus on during the Hard Economic Times

To ensure the business’ survival, longevity, and growth, SMEs are advised to identify and promptly address the most vulnerable areas:

- finance

- operations and business models

- people and processes

Finance

First of all, focus on internal resources and capabilities. Business owners should know the precise amounts they need to put into the business and to meet the operating costs, as well as their cash projections.

To ensure long-term viability, it’s imperative to promptly build up a cash emergency fund and make significant cuts to every aspect of the day-to-day business operations.

Start by cutting all non-core projects and underperforming departments. Cut marketing and sales spending until your customers are in a position to be buying again. Cut all contracted help you can do without.

Identify your incurred costs and conduct negotiations to minimize the direct and indirect costs. Use the economic situation as leverage when negotiating rent, equipment leasing agreements, etc.

With many employees already working from home, many SMEs should consider whether they truly need a physical space. If they establish an entirely remote workforce or switch to flexible coworking office spaces, they can cut overhead costs significantly.

Go digital wherever possible. For example, modern technologies minimize the need for brick-and-mortar stores, contact centers, support service, business travel, employee training at the office, etc. It’s pretty easy to build a small business website quickly.

When economies are in a volatile state and credit markets are tight, it is best to minimize the company’s reliance on traditional external funding. Look for sources of funds that are non-equity. For example, government grants that prioritize SMEs, startups, and entrepreneurs are becoming available on a global scale. Explore the Small Business Administration programs and other government stimulus packages. Don’t miss the opportunities when governments allow businesses to suspend payments of selected social charges and taxes, or take other steps that can provide much needed monetary relief.

The global crisis and local quarantines and lockdowns foster various partnerships and alliances. SMEs may form complementary alliances, tapping into each other’s resources and capabilities. Crowdfunding, peer-to-peer lending networks, and lending clubs can help fill the void created by the credit crunch. Bartering with other businesses is another way to lower your operations costs, and it makes sense to consider short-term deals that you wouldn’t think of doing before the crisis.

Business Model and Operations

SMEs need to stay flexible and adapt to the new climate. This includes adjusting their current business models, using opportunities to gain competitive advantage, and more. It may be that the economic slowdown finally provides you with the opportunity and enough time to come together as a team (albeit virtually) and evaluate the work you have done thus far. SMEs are blessed with the benefit of fast decision-making and an agility that allows them to restructure, recalibrate, and re-innovate quickly.

The three Rs to address are reflection, research, and relations:

- Reflect on the wins and the failures and identify the strategic solutions and approaches that were most effective.

- Research your customers and competitors to understand the shifting audience and market demographics with an eye on finding new solutions.

- The relationships you build with others in the industry and the discussions you participate in can form connections and potential business partnerships down the road, keep you updated on new trends, technologies, ways of solving problems, and smarter solutions to adapt to this new reality.

It’s also high time for better relationships with your wholesalers, as well as recalling who actually uses your product or service. Ask for more detailed information on who your end-users are. If you understand what is going on with them, you can better connect the dots between the economy and your business.

Research the change in the market demand and consumer behavior, as well as the possible gaps and opportunities to benefit from. Then re-evaluate your propositions and business models. Revise your revenue goals and product timelines, create a new business model along with a matching operating plan, and ensure clear and constant communications with the market and investors.

B2C businesses may explore the possibility of switching to the B2B2C model. While consumers react immediately to economic fluctuations, organizations work on annual budget cycles and must keep spending to keep operating.

Still, be aware that most businesses and government clients may go into survival mode for at least six months. Unless your product or service is the cornerstone of their operations, you should expect that some of your contracts will be canceled.

Develop honest and constant communications with your current clients. Help them and be there for them when they need you most, which may start with adjusting price points and payment terms.

Consider diversifying your revenue streams and customer segments. If your business is consumer-focused, a new distribution model via companies might work. You may find new consumers among affluent populations that are less sensitive to economic jitters. If your business is enterprise-focused, you might cater to those who need your service for survival, especially now, and target the more financially resilient larger enterprises. The key to a diversification strategy is a timely exploration and thorough understanding of your business’s subtle signals.

Explore innovative and even radical ways to obtain new customers and deliver added value to the market. This can be realized by fine-tuning and tailoring current services and by developing new lines of offerings according to current demand. Take time to understand your customers’ needs and invest in top-notch customer success. If you manage to make your product mission-critical and indispensable, your customers and partners won’t cut it even during a recession.

Focus on projects that will facilitate the long-term success of your business. If your flagship product sales are unlikely to speed up until the economy resumes growing, it makes sense to redirect some or all of your business efforts towards another project.

If you can contribute to alleviating the COVID-19 problem, try to do so. Examples of such projects can be tools for easy work from home, live streaming, online learning and consulting, mobile apps for staying fit and healthy, or whatever can help solve people’s problems in these difficult times.

Exporting may help SMEs become more economically diverse and robust. It is suitable not just for food or retail businesses. One of this global economy’s upsides is that there is a buyer out there for anything you’re selling. Services are also in demand globally, for example, engineers and environmental and architectural companies. However, beware of the currency risks, insurance and shipping costs. To help you navigate exporting, you can get free help from a SCORE mentor who understands the nuances you may encounter.

Market smartly. Here, technology offers numerous ways to save money while increasing profits:

- You can expand your market by selling through a website, a mobile application, chatbots, social networks, and other channels;

- Email marketing is cheaper than electronic or print advertising;

- If you optimize your website for search engines, it will be coming up at the top of your customers’ searches;

- You can produce affordable marketing materials in the format of podcasts or webinars;

- An online customer loyalty program updating consumers on sales, discounts, referral bonuses, and coupons will keep them engaged.

Conduct competitor analysis regularly. Monitor your competitors’ actions and study their promotional techniques. Did they modify their products or сut the prices? Are they using fresh marketing tactics? Identify the regions or potential customers that they avoid, overlook, or have failed with. You might seize the opportunities they missed. If you are exceptionally lucky and your competitor is not, you may even acquire them without cash in an all-equity deal, which was unthinkable in a strong economy. Experienced business owners recommend thinking ahead of time about which companies you would want to buy and for what purposes.

People and Processes

In the new context, SMEs need to ensure their teams’ safety, health, and productivity during economic and employment uncertainty while slashing budgets.

The first step is to help team members feel safe, empowered, and committed. Trust, empathy, and availability of the company leaders play a crucial role in creating an environment where employees welcome new changes, work productively, and want to put in the extra effort. Even finding time to listen to their concerns and needs goes a long way. Investing in employee wellness and boosting morale promote productivity and motivation throughout these indefinite periods of working from home and widespread panic.

Employees need to believe that a strong leadership team is making smart strategic choices and steering the business through unfavorable economic conditions. For active and transparent communication between the leadership, investors, and staff, build new platforms and encourage regular conversations between all stakeholders. Such communication promotes the exchange of valuable guidance and helps with making smart collective decisions.

Provide everybody with the tools for internal and external communications, remote working, and other essential processes. This long-term investment helps safeguard businesses from any turbulence that may come.

Unfortunately, some executives will be forced to decide which of their employees are indispensable and which are not. Superstars of employees are hard enough to find. Taking a temporary pay cut in extraordinary circumstances may be the only way to hold on to your best talent and ensure the viability of the business. Try to keep them even if it means taking temporary salary reductions in exchange for more equity in the company. Some companies reduce the number of work hours. If the employees are really committed to your mission, they will be looking for a way to stay, too.

Be realistic about possible employee benefits. It’s better to cut the perks now and add them when your revenue grows than to promise too many and eventually fail to maintain them.

However, leaders can’t ask employees to take a pay cut and not do the same. Leading by example is critical for keeping everyone focused and motivated.

Those team members whom the executives deem less vital for the enterprise may need to be laid off. However, consider the cost of severance packages and litigation risks, as well as the hit on the remaining team’s morale. It’s better, whenever possible and if resources allow, to look for alternatives. For example, you may shift an employee in question to other tasks or ‘exchange’ them with a partner firm.

If critical vacancies occur, you may fill them at a significantly lower cost by outsourcing the work. The availability of various freelancers will grow alongside the unemployment rate. They will be much more affordable to hire than full-time employees and will not ask for perks.

Advice for Startups

- Startups mainly die because they run out of cash. Develop a financial backup plan for your business and personal finances if you fail to hit your initial revenue projections. Put in place a plan to build up cash reserves so that you have at least 12 months of cash. Budget carefully so you can continue making crucial payments. Finally, check your bank balance to make sure you are ready to start a new venture.

- Manage your expectations and expenses by starting small and planning to expand when your business takes off. Review your business plan and reconsider your needs. For example, identify the most affordable office space or just stay virtual for a while.

- As for staffing needs, put off hiring full-time staff and instead try to fill positions with independent contractors, temporary and part-time employees, or even outsourcing some tasks.

- Startups that rely on infusions of venture capital investment should expect that VCs will be restricting their new deal activity. If you were in M&A negotiations, don’t expect anything to happen until the pandemic ends. Your existing angel investors may help a bit, but expect it to be quite costly.

- Trajectory-based financing is another option. Capital firms provide unsecured loans based on predictions of future business trends.

- Before applying for any loan, ask trusted friends who are business owners, an accountant, loan officer at the bank, or professional advisors to review your business plan to make sure you don’t make inaccurate assumptions or overlook anything critical. It may turn out that taking on excessive new debt is not practical, as debt services can bring you down.

- Communicate regularly with your shareholders, giving them the good and the bad news.

- During economic downturns, more creativity is required to get ahead of the game and competitors. Think about ways to broaden your business appeal and customer base. Alternatively, you may divide your original customer base into smaller segments so you can market more strategically, e.g., targeting consumers within a specific age range, career type, income level, or geographic location.

- Many startups possess valuable core in-house capabilities that are in demand across many industries: software development, data analytics, artificial intelligence, blockchain technology, cybersecurity, etc. Consider changing your startup’s course by marketing activities that may prove more profitable in the new climate.

If you wish to learn more about managing a startup during hard economic times, there is a fresh and free detailed ‘recession playbook’ prepared by First Round Capital.

The Bottom Line

Economic factors relate to the global economy but have a profound effect on the inner-workings of every company. The COVID-19 pandemic started as a health crisis, then became an economic concern, and now has resulted in a recession affecting companies and employees worldwide.

Small businesses and startups that lack access to financial and equity markets and government support may face particular challenges during a recession. It is vital for them to be agile and to recession-proof their finances by restricting spending and debt while diversifying their income. They should start by analyzing the market and industry changes, developing a plan to scale the business, and transforming the operating model and processes.

While the impact of recession on businesses can be severe, it’s critical not to let fear and uncertainty sidetrack the business decisions. Adversities are a great litmus test for entities’ flexibility and resilience and are challenging them to broaden their horizons and become more innovative. There are unique benefits and opportunities as well associated with starting and conducting business during an economic downturn. If entrepreneurs do their homework, think strategically, leverage technology, and minimize costs while maximizing the value added for customers, they can seize the opportunities to build a foundation for long-lasting business success.

And another piece of advice: stay optimistic. Right now, you may see the numbers only getting worse, but it’s possible that your team will do some of its best work over the next few months and will come out of the downturn more robust than before. Recessions come and go, and we are likely to live through a handful of them during our lifetime. Even the Great Depression eventually ended and was followed by arguably the strongest economic growth period in U.S. history.

Content created by our partner, Onix-systems.